Aspen Aerogels Inc. - ASPN

Some final thoughts

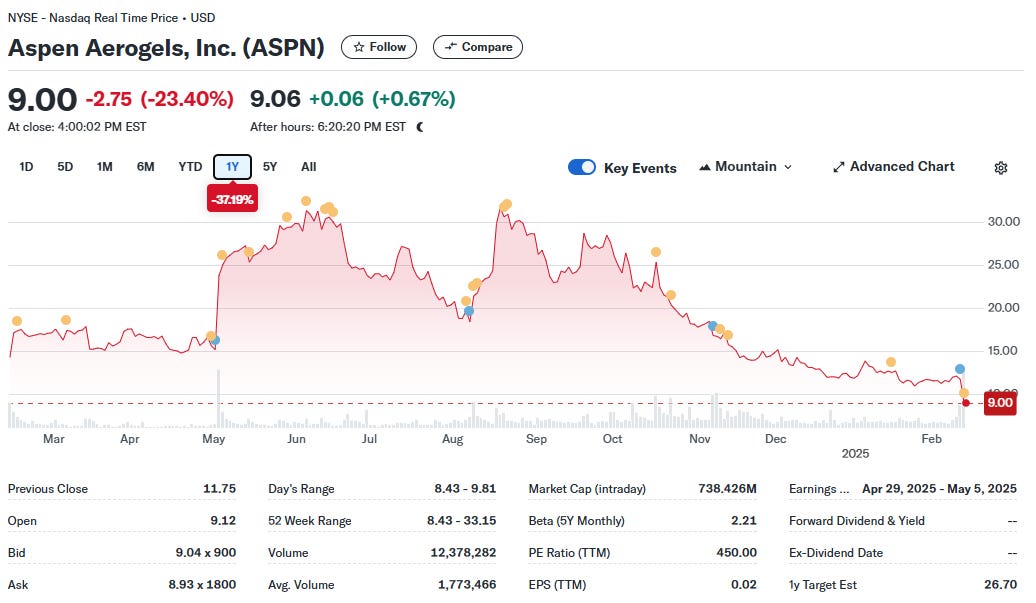

I have been pointing out signs since last May that not all was going well for the folks over at ASPN. Despite announcing what appeared to be some bullish quarterly results over the past several quarters, shares have proven to be incredibly weak over the past several months and culminated in today’s total collapse.

Though I removed these folks from my year-end interest list and was ready to move on to other names, I thought I would add a few thoughts and point out a couple of tidbits from the company’s Q4 2024 earnings release and conference call in case anyone out there was considering doing some bottom fishing.

While Q4 revenues exceeded analyst estimates by maybe $3M, the revenue mix was likely a bit of a shocker to most. Thermal barrier revenues suffered their first sequential decline in 2 years while Energy Industrial revenues were up more than double. Despite the company saying what a great business the Energy Industrial vertical may be, investors don’t really care about it. This story is all about EV’s and their Thermal Barrier business.

Guidance for Q1 2025 revenues was rather weak, and at best will be about even with Q1 2024, and at worst will be down over 20%. The company blamed the shortfall on General Motors and their inventory of EV’s that they hope will decline and lead to a pickup in volumes in later quarters. Just a reminder that higher interest rates, removal of EV mandates, and a reduction in EV incentives may all lead to some drastic and unanticipated changes.

“Our guide for Q1 reflects what we believe is a temporary drop in production to reduce finished vehicle inventory levels. With an annualized sales rate in the U.S. of over 270,000 vehicles in Q4 of last year, and market share of 19%, it is fair to expect GM to increase production after Q1 to meet its targets and launch 3 additional nameplates.”

The company is targeting 300K vehicles through the GM/Honda/Acura partnership, which is not that much more than the 275K or so produced in 2024, and even that appears to be somewhat in doubt. So while 2024 turned out to be a nice surprise for them, 2025 will be decidedly more flattish.

“I mean if GM gets to 300,000 vehicles plus more, if we actually include the Honda and the Acura nameplates will be ecstatic, right? It will be a better year than last year. That's just not what we're seeing in Q1.”

Why should General Motors and this business with Honda/Acura matter so much?

Because in FY2023 GM was responsible for 42% of overall revenues (a second (Honda/Acura) was 14%), and in FY2022 they were 25% (second was 22%). While we don’t know the number for FY2024 quite yet, through 9 months they had 2 customers responsible for a combined 74% of overall revenues, so the concentration from the GM partnership appears to be growing much higher.

(By the way, here’s a fun exercise. So we know their top 2 customers are related to the Thermal Barrier business and not the Energy Industrial vertical. Take a wild guess at what percentage of overall revenues the Thermal Barrier business was through the first 9 months of FY2024? If you answered 74%, or exactly what their top 2 customers reported, then give yourself a pat on the back. Currently ALL of their Thermal Barrier revenues appear to be coming from this single source.)

The company did announce on their conference call and in their release that Volvo’s commercial trucks program has qualified them, and they have announced in the past that Porsche’s 718 EV and a deal with Stellantis and Mercedes Benz, but as of yet, those programs don’t appear to be contributing to the company’s revenues.

Other than being their largest customer, the GM relationship is also a bit special and somewhat tangled in other ways. The company took care to mention the following fact not once, but twice on the earnings conference call, which I at least found to be somewhat odd:

“Let me be crystal clear. We're talking about finished vehicle inventories at General Motors, where we are single sourced, not pirating inventories in the value chain, which we have full visibility on GM had a strong production ramp in 2024 and is targeting over 300,000 vehicles in 2025 if we include the Honda and Acura nameplates.”

And then there was this mention.

“While our Q1 outlook does not reflect that pace, we are prepared to meet it as General Motors sole source thermal barrier supplier. With a strong foundation in place, we are confident in our ability to adapt, innovate and capture significant opportunities in 2025.”

I added the bold to the above quotes.

I don’t remember the company ever explicitly mentioning that phrase in any of their prior conference calls, and yet it was mentioned twice on this call. Interesting.

Ordinarily being the sole source provides some comfort for a company, and higher margins, which is why most companies tend to have multiple sources. Should GM ever opt to qualify an additional source, it could also be a source of problems for ASPN, and considering their large revenue concentration, be responsible for a potential revenue decline.

Any reason to believe that may happen anytime soon?

Well, there was that odd financing arrangement that they entered into with MidCap Financial back in August. MidCap provided them some cash and a line of credit, while at the same time ASPN shut down a cheaper $100M credit facility that they had open with none other than General Motors. I put some thoughts down about the tangled arrangement back then.

Reading back through the prior calls, it strikes me as a bit odd that none of the analysts chose to question the whole financing arrangement with MidCap or consider asking the company why they chose to shut down a financing avenue with their largest customer. Seems like a natural question to me at least.

The company is making an effort to reduce their operating expense profile, and they are also attempting to reduce the CapEx burden that has been holding them down over the last, well, ever since they decided to build an additional facility out in Georgia. Now that that’s apparently off the table and they’re repurposing the equipment that’s already there to other facilities, they are talking up the possibilities of what to do with all the extra cash they’re about to have. Stock buybacks? Acquisitions? It all appears on the table.

With shares trading at their lows and the EV landscape looking just a tad murky, they may be getting ahead of themselves by just a bit.