U-BX Technology Ltd. - UBXG

If the markets worked better, we wouldn't find such interesting companies!

Well, my broker is EF Hutton, and EF Hutton says...

Not to age myself, but I still remember those commercials, where a couple of people would be sitting in a crowded room, discussing the stock market, when one turns to the other with that nifty catchphrase and the whole room quiets down and everybody leans in to hear what the EF Hutton broker has to say.

I doubt the prior EF Hutton management team (going back,, oh, maybe 40 years or so) would have ever been involved in a company like UBXG, but the new owners of that particular piece of financial history apparently have no such compunction or issues with whatever business happens to walk through their front door.

If this description in Wikipedia is correct, EF Hutton’s most recent iteration was brought back to life in 2021 by the joint efforts of UK-based Kingswood Holdings and US-based Benchmark Investments LLC, the latter of which was subsequently purchased in 2023 by the newly Christened EF Hutton Group that they themselves had helped launch. Sorta a delayed reverse merger into what was hoped would be a more popular shell, if you will. Hard to believe that almost 40 years after the name was unceremoniously retired that somebody considered it a good idea to bring it back.

What type of company happened to walk through EF Hutton’s doors?

One of those that US-based investors will likely never have any hope of getting their investment dollars back out of. Their description.

U-BX was incorporated on June 30, 2021 in the Cayman Islands. U-BX does not have material operations of its own. We conduct business through the PRC Operating Entities. Since U-BX Beijing’s establishment in 2018, the PRC Operating Entities have focused on providing value-added services using artificial intelligence-driven technology to businesses within the insurance industry, including insurance carriers and brokers. All of our revenue was and will continue to be derived from mainland China, and none of our revenue was derived from Hong Kong or Macau.

A 100% mainland China operating business with no plans on exporting their business model anywhere else. Sounds fairly standard.

And the ownership structure? Also fairly standard. Here is a map that they include in their filings. Notice the tiny sliver devoted to “IPO Investors” in the upper right corner. Of the 2.3M shares the company sold during their IPO back in March for $5 a piece (they had originally filed to sell 6M shares back in 2022), there are another 25M shares owned by a trio of BVI entities that in turn are owners of what is supposedly the (non) operating Cayman Islands company which in turn has a special contractual relationship with a Hong Kong entity which in turn owns a variety of PRC-based operating businesses which are the true source of revenues for everything that the company says that it does. Because in the end, when this thing is trading for pennies and US investors once again figure out that they have been swindled and the SEC has done nothing to protect them, it’s this ownership structure that stands between them and any hope of getting a payback.

What these folks actually do isn’t clearly evident from the description that they provide in their public filings. They spend a lot of time talking about "risk assessment services” and their “magic mirror” algorithm that is supposed to help auto insurance carriers calculate the payout risk for every person who applies for a policy based on the car they drive and where they drive it. In fact, in their prospectus, the “magic mirror” phrase is repeated 44 different times, so it must be important. They also supposedly engage in “digital promotion services” on behalf of these insurance carriers and “value-added bundled benefits” rounds out their 3 main business focuses. It’s a bit long, but here’s how they describe it all:

Our PRC Operating Entities’ business primarily consists of providing the following three services/products: i) digital promotion services, ii) risk assessment services, and iii) value-added bundled benefits. The PRC Operating Entities help their institutional clients obtain visibility on various social media platforms and generate its revenue based on consumers’ clicks, views or its clients’ promotion time through those channels. U-BX Beijing also developed a unique algorithm and named it the “Magic Mirror” to calculate payout risks for insurance carriers to underwrite auto insurance coverage. Utilizing the proprietary algorithmic model, our PRC Operating Entities are able to generate individualized risk reports based on the vehicle brand, model, travel area, and vehicle age. In turn, our PRC Operating Entities are able to generate revenue based on the number of assessment reports provided to the insurance carriers. Lastly, to help major insurance carriers or brokers attract their customers, our PRC Operating Entities sell bundled benefits, including car wash, maintenance plans or parking notifications, to these carriers, which they may then pass onto their customers for either low or no cost.

In addition to servicing institutional customers, our PRC Operating Entities provide up-to-date insurance-related information to individual consumers through its mini-application embedded in other social media platforms. The information is provided to educate consumers and insurance brokers about the insurance industry, thus helping us build a stronger brand image with the general public.

At present, our PRC Operating Entities’ client base consists of more than 300 city-level property and auto insurance carriers nationwide, in addition to approximately 200,000 insurance brokers that use its products and services to conduct business on a daily basis. Some of its clients include large corporations such as the People’s Insurance Company of China, Dajia Property Insurance Co., Ltd., China Pacific Property Insurance Co., Ltd., China Life Property Insurance Co., Ltd., Yongcheng Property Insurance Co., Ltd., Huatai Insurance Brokers Co., Ltd. With the future digitization of the insurance industry, we expect to have a broader reach within the overall insurance industry, as our PRC Operating Entities’ business focuses on providing insurance technology solutions to insurance carriers interested in applying artificial intelligence technology and online traffic promotion method in their operation. We believe the future digitization of the insurance industry will create more interest among insurance carriers in using the technology and promotion channels our PRC Operating Entities offers.

Until you read that part of car washes and parking notification, it sounds like some sort of a technology outfit that helps insurance carriers figure out who is worthwhile to underwrite based on the type of car they drive and where they drive it, all using some sort of AI powered secret sauce that they refer to as “magic mirror.” Then on the side they have some type of business that they call digital promotion services which apparently is a paid click type of service and also they offer some additional value-added products like coupons for car washes. According to their prospectus, they’ve got 8 web sites that help generate revenue.

Perhaps you’ll have better luck than I, but the first 4 web sites all seemed to take me back to the u-bx.com landing page, and I wasn’t able to pull up another 3 of their web sites which for one reason or another just gave me an error message loading. Yet another had some information on building a web site, but with very rudimentary information. And all of the web sites that I was able to pull up, they took forever to load and clicking on links that were sometimes broken or also took forever to load. Overall, a fairly frustrating experience that, much like hearing EF Hutton, took me back 40 years to web pages loading over a twisted copper landline connection (slowwww).

The next step was looking for the financials, where I was bracing myself for the usual low revenue, high R&D spend, growing losses that an outfit like this typically sports. Let me just say up front that, boy, was I wrong.

You don’t have to look very hard at the company’s financial statements to get the feeling that something is just not right. Like most of these “Chinese Hustle” types of names, they came public in March 2024 but the most recent financial statements they presented at the time date back to June 30th 2023. So there were a solid 9 months worth of operations happening and which they did not disclose by the time they opted to take US investor money, giving them ample time and room for some pretty serious shenanigans. So when I say something is not right, I mean something is downright horrible.

Their revenues at the end of June 2023 were supposedly $94.3M, up slightly from $86.7M in 2022. Go back to their original old F-1 filing back in January 2022 and you see $72.4M in FY 2021 and $62.6M in FY 2020. At first glance, that was something of a surprise. Wasn’t expecting a big number at all, or the nifty little ramp. You know what else is a surprise? Despite leading off their prospectus with the standard dollar/RMB exchange rate information, you won’t find a single financial statement using RMB in the entire document. Sure they have some government required numbers that are denominated in RMB, but everything else is spelled out in dollars, almost as if this company and offering was tailor made with the US investor specifically in mind.

Glancing down a bit further and you notice the COGS and gross margins, and when you pair it together with the balance sheet that I’ll show in a moment, then it all starts to make some sense. Those are COGS and gross margins more in line with some sort of distribution business rather than what is supposedly some sort of technology outfit. Back when they used to have these things called pre-paid phone cards, there were companies out there would buy a crap ton of phone minutes from one of the majors (AT&T, Verizon) in the hopes they could re-sell them for a fraction of a penny more. They all had huge revenues but teeny tiny gross margins that for some reason investors thought would be able to grow.

But they’re also a sign of a potential gross/net revenue reporting, which is likely what is happening here. For example, in their “value-added services” segment, if somebody clicks a coupon for a car wash and UBXG gets, say, 25 cents for every person they refer to that business and the business charges $20 for a car wash, then UBXG is booking the entire $20 and counting the $19.75 as part of COGS rather than simply booking 25 cents worth of revenue. Or maybe they get $1 every time somebody using their “magic mirror” app actually buys an insurance policy, but then they recognize the entire policy amount as revenues.

G&A expenses are the only one’s listed, and there is no R&D expenditures whatsoever, so the 60% of proceeds from the IPO that the company claims will be spent on R&D will apparently be the first dollars they spend on R&D in quite some time.

How do they break down revenues between those 3 business verticals?

So far those are all numbers that investors had to go by when they invested in their IPO. It was all just so impressive that the company’s CFO at the time of their IPO, a Ms. Xiaoli Zhong, resigned a month or so later. Apparently not due to any disagreements with the company or with their auditors Wei, Wei, & Co. of Flushing, NY, but that’s all fairly standard language.

But then, what should just make everybody’s blood boil, a couple of months after taking US investor money, and maybe a month after their prior CFO opts to resign, they come out with their unaudited 6 month financials through December 2023, because, yeah, that’s all your US SEC requires of companies like this.

Revenues DOWN 48% year over year while operating expenses were naturally 24% higher as they readied themselves to take all of that easy US investor money. And they guaranteed knew all of this at the time they were trying to come public.

And how widespread was the carnage? Primarily in that top business or across all of their businesses?

Looks like their coupon clipping business isn’t doing all that horribly, but the paid for clicks business and the “magic mirror” businesses are in the dumps.

And what does the stock do during this revelation that their business is down 48%? Volume triples the day they file their 6-K and the shares double over the next month. Now there’s a set of rational buyers for you.

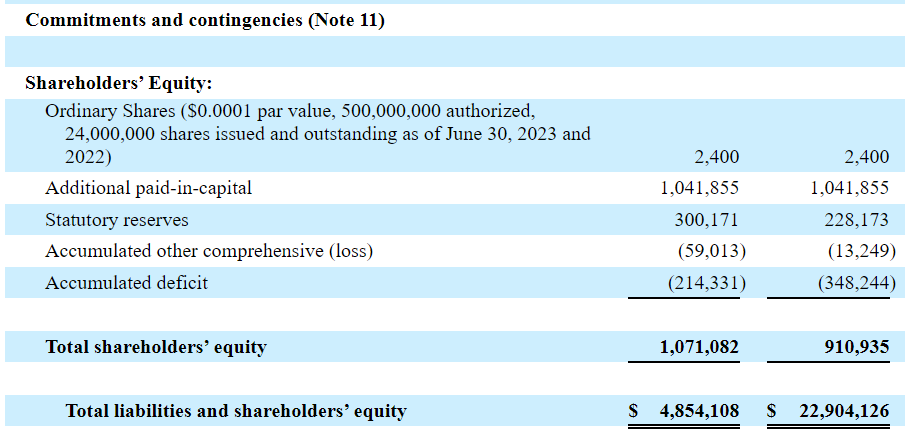

And how about the balance sheet that is being used to fund upwards of $100M in annual revenues from 300+ insurance carriers and 200K+ insurance brokers? Well, they didn’t include one with their mid-year update, but they did have one in their prospectus.

No balance sheet to speak of, and the largest item on the balance sheet by far (advance to suppliers/advance from customer) has only this mention in the section on operating cash flows. I mean, less than $4,000 in total PP&E for a “technology” or “marketing” company? Really? That’s like 2 laptops, a printer, and a couple of desks for the “9 employees on our research and development team.” What a joke.

b) decrease in advances to suppliers of $16.6 million was due to we made payments to our suppliers in advance in order to have a lower purchase price since our customers made payments in advance to us as of June 30, 2022; c) decrease in advance from customers of $18.4 million was due to our customers made payments in advance whereas the service was not delivered as of June 30, 2022.

To which you just gotta ask: who would be willing to pay these guys $21M UP FRONT for anything these folks have to offer, and what exactly do they have to offer that would necessitate any kind of an up front payment? What type of “suppliers” can this type of an outfit have? Coupons? Insurance assessments? Perhaps pay-for-clicks? Must be some national digital marketing campaign that earns them a 1% gross margin?

And apparently that didn’t all come from a single customer either:

For the year ended June 30, 2023, one customer accounted for 12.5% of the Company’s total revenue. No customer individually represents greater than 10.0% of total revenue of the Company for the year ended June 30, 2022.

The 12.5% customer would have been worth maybe $12M in overall revenues, but the advance from supplier at the end of FY 2022 was almost $21M, and that customer was not big enough in 2022 for them to make any mention. So a group of customers decided to band together and pony up $21M in advance for their services, at which point the company went to several suppliers and placed some orders on the customers behalf, all while earning that outsized 2% gross margin. Sound about right?

For the year ended June 30, 2023, two suppliers accounted for 20.4% and 14.2% of the Company’s total purchases. For the year ended June 30, 2022, three suppliers accounted for 20.7%, 17.8% and 11.8% of the Company’s total purchases.

This from a company with a little over $1M in cash on their balance sheet and total assets (if you exclude these ludicrous entries) of maybe $2.5M.

Back in the 2022 time period when the company was at first hoping to come public, they did a couple of private share offerings for cash. This was the time when they were going to be announcing their $86M revenue year and they were supposedly a hot technology stock. The price for the shares? The first 7.5M share tranche was done for fractions of a cent, while the second 1.032M share sale was done for maybe 89 cents a share, and to date, is primarily responsible for all of their paid-in-capital.

That 89 cent number sounds like a more reasonable price target than the current share price north of $13 these shares are currently receiving.

Finally, the official short interest on this thing is only 33k shares, and they did sell 2M on the offering, so perhaps a few shares are out there somewhere to borrow. There are no institutional holders of note, so perhaps shares would show up in some more retail oriented locations.

The lockup period for the stock is a full year, so in a perfect world you shouldn’t see any management stock until next April, but then there are those odd days like last Tuesday, August 6th, when this thing suddenly decides to trade 4M shares on zero news and it all makes you wonder.